Marketing Managers

Demand Trends for the Canadian Market:

April showers brought with them slowed demand as more people chose to stay in place and the market as a whole showed little movement. Typically April sees continued growth in renter demand as the weather gradually improves and renters re-emerge to make housing decisions anew. Unfortunately, this year saw a dip in overall demand and a reversal in the long-standing trend of tightening market conditions.

The number of renters in the market for a new home decreased at a rate 1.8x higher than the decline in property availability suggesting that the market experienced some softening. Conversely, those renters who remain in the market for new accommodations are actually ramping up their activity with average leads per user increasing for the fifth consecutive month.

Nationally demand scores are down -1.6% between April and March, with properties down -1.8%, and unique prospects down -3.3%. As a whole the market experienced a slow start to April however leasing activity picked up once again towards the end of the month in line with the for-sale market.

While progress remains slow, this mild decline in demand was not felt equally across the country with the top 10 markets made up primarily of secondary communities across Ontario and British Columbia in fact showing strong growth with demand scores up +7.3% and directly attributable to the inverse movement of properties (-5.6%) and renters (+1.2%). With more people heading back to work in the office, we expect to continue seeing a trend of renters being attracted to secondary markets which offer many of the benefits of primary markets, without the drawbacks of a higher cost of living.

Although too early to tell where the market will lead, we expect the overall lead trajectory to regain its upwards momentum and grow through May.

Below we will identify notable changes in rental demand, highlight market-specific trends, and discuss what the coming months may look like for the rental demand in Canada.

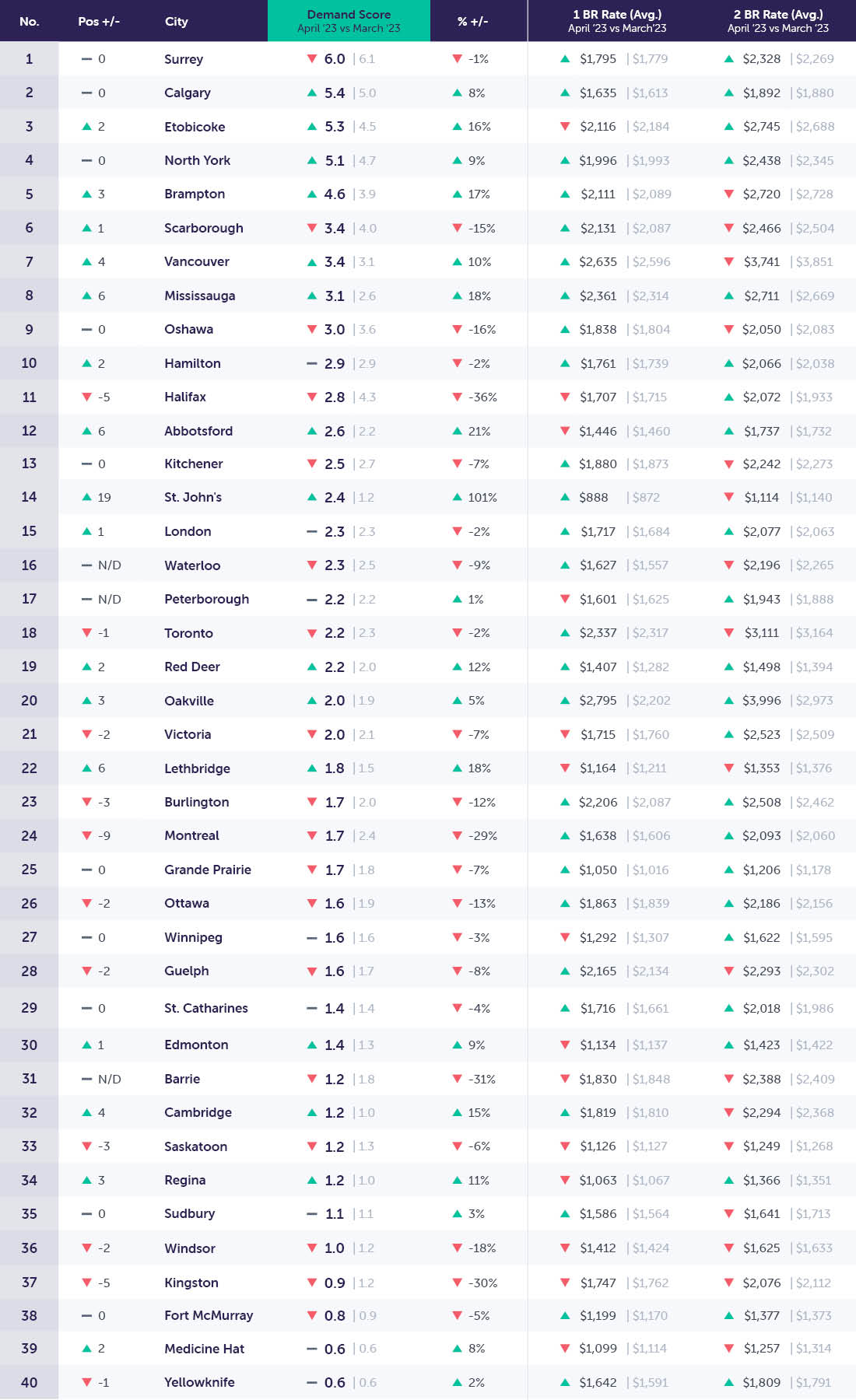

Top 40 Canadian Cities in Demand

Notable Changes in Demand Over the Past Month

April saw little change in overall demand scores with a mild dip relative to March. Renter activity slowed marginally relative to March due to a decline in unique renters across the country. Notable markets this month include Burnaby, which fell out of our rankings due to a decline in available properties, Vancouver which gained 4 spots and is now ranked 7th in our list of markets, and Halifax which practically switched spots with Vancouver by going from the 6th spot in our rankings to 11th. Western Canada continues to showcase strongly in our top 10 list of markets displaying the strong continued growth in the rental demand experienced in Western Canada.

Month-Over-Month (M/M)

- Primary: Demand scores are down -1.3%

- Secondary: Demand scores are down -4.7%

- Tertiary: Demand scores are down -0.1%

Month-over-month (M/M) National demand scores are down by -1.6% in April 2023 compared with March 2023. Stalling the strong growth experienced in March and delaying the summer start of the summer leasing season.

Year-Over-Year (Y/Y)

- Primary: Demand scores are down -15.1%

- Secondary: Demand scores are down -45%

- Tertiary: Demand scores are down -24.7%

Year-over-year (Y/Y): National demand scores are down -24.2% in April 2023 compared with April 2022. Demand scores continue to trend downwards annually for the sixth month in a row. Primarily due to the strong leasing activity throughout 2022 which has since cooled once the pent-up demand of the pandemic period was finally met. Demand scores don't paint the full picture however as unique prospects per property are relatively flat down 0.8% year-over-year. This leaves properties in a very similar position when attracting quality tenants and enabling them to maintain strong lead volumes regardless of the general trajectory of active renters in the market.

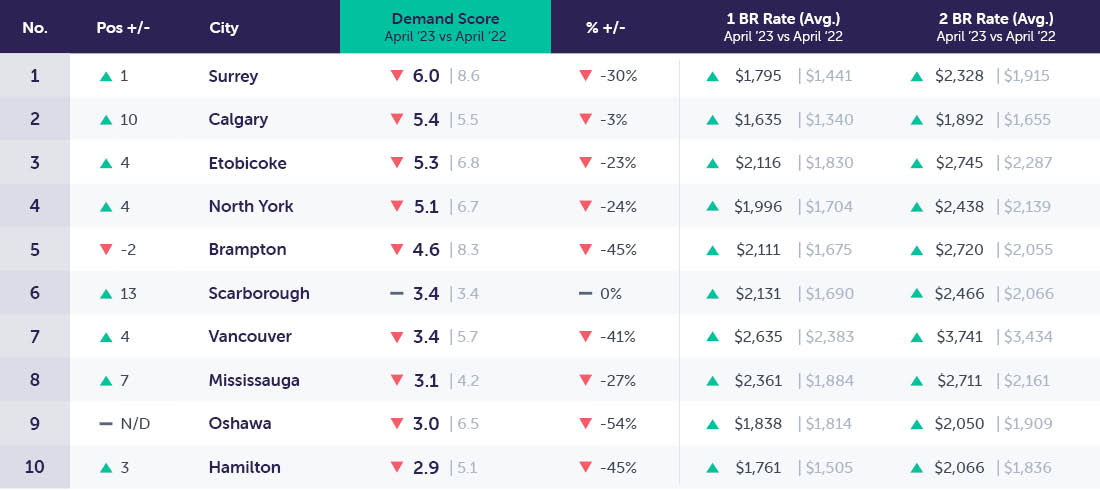

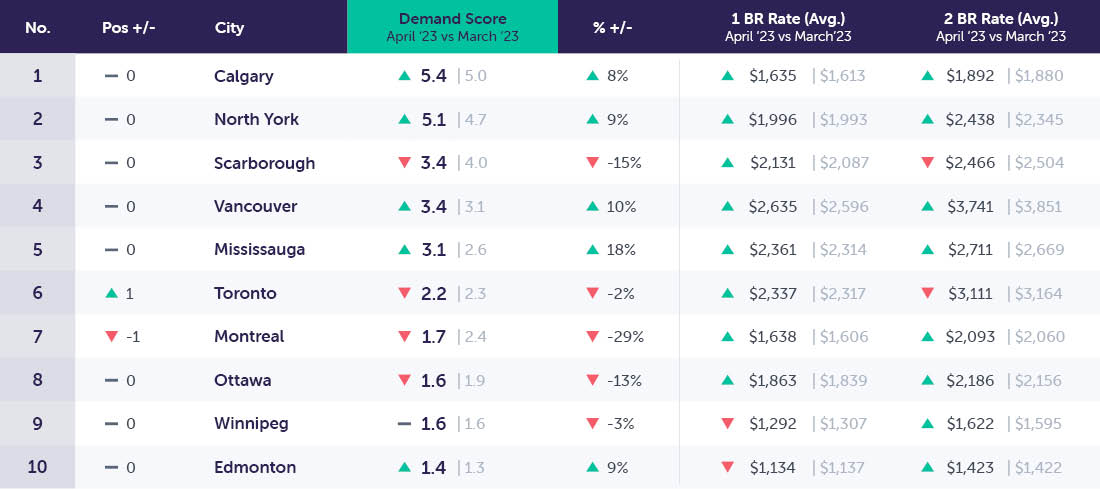

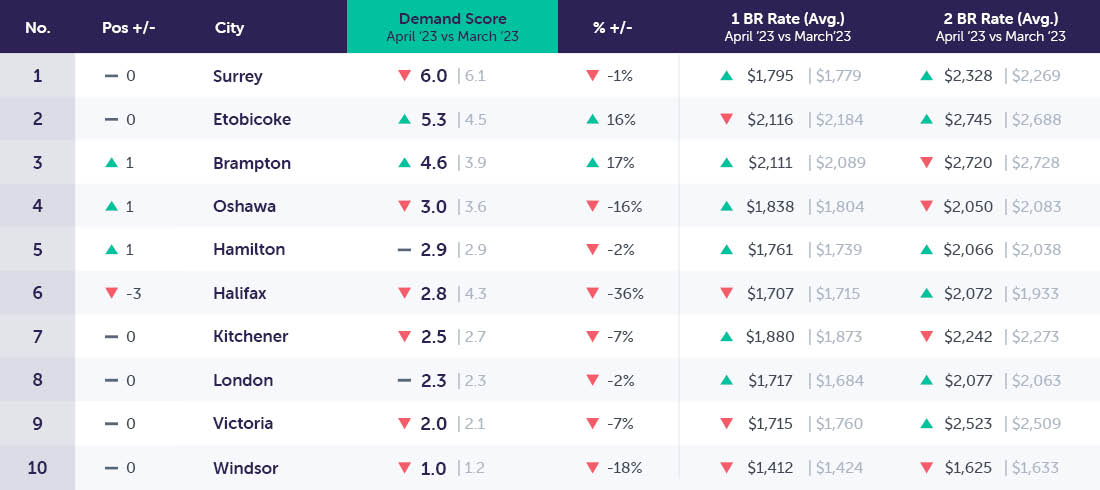

An Analysis of The Top 10 Canadian Markets:

Top 10 Canadian Cities in Demand Drill Down (M/M): April 2023 vs. March 2023

Key Trends for Top 10 Canadian Cities in Demand (M/M)

The top 10 markets show signs of ongoing growth, unlike the remainder of the Country. With a monthly increase of +7.3% in overall demand scores and an increase in unique prospects of +1.2%; these communities show signs of continued tightening and greater competition amongst renters for an ever-dwindling market of available units. Average rents continue to trend upwards albeit slowly up +0.9% month over month for one-bedroom units for the second month in a row.

Part of this rent growth is likely attributed to a survivorship bias with more moderately priced units being leased first and leaving more premium units on the market for longer.

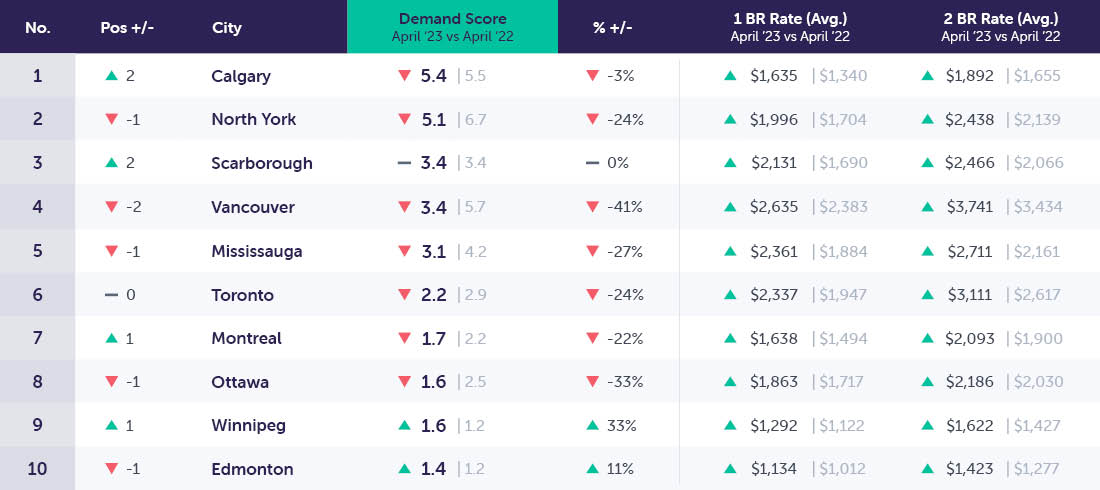

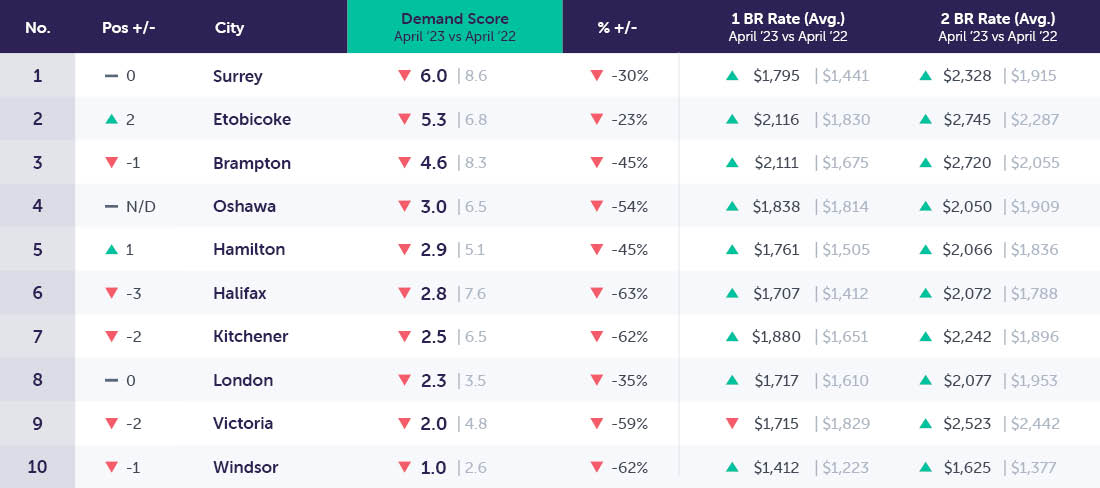

Top 10 Canadian Cities Drill Down (Y/Y): April 2023 vs. April 2022

Key Trends for the Top 10 Canadian Cities in Demand (Y/Y)

Year-over-year the top 10 markets experienced a decline of -30.4% in demand scores. In line with this decline for the first time in recent history; year-over-year renter counts have actually declined at a greater rate than available properties. This resulted in average prospects per property decreasing by -8.9% year-over-year which in turn suggests that these markets may have finally reached peak occupancy or as close to it as possible and that the competition amongst available properties will in fact increase as there are fewer renters to property availabilities.

This however does not paint a full picture of the current situation of these markets as several of these communities have experienced quite substantial shifts in their rankings thus suggesting that they are experiencing vastly different conditions to those of 2022 and not likely to any detriment.

An Analysis of Key Canadian Markets

To better segment our data and analyze what is happening within specific markets across Canada, we have broken down the rest of our data into 3 key market segments:

- Primary (Populations Over 600K)

- Secondary (Populations Between 600-235K)

- Tertiary (Populations Between 235-100K)

Here we will gain a deeper perspective on demand across larger population centers and trends in various markets.

Primary Markets (Populations >600K)

Primary Market Drill Down (M/M): April 2023 vs. March 2023

Notable Changes in Primary Markets Over The Past Month

*Overall demand scores are down -1.3% month-over-month, unique prospects are down -2.6%, and properties are down -1.4%.

Primary markets experienced more muted effects in April and remained roughly in line with conditions experienced in March. With half the markets show positive growth (Calgary, North York, Vancouver, Mississauga, and Edmonton) with an overall average of +10.8% growth. The remaining markets (Scarborough, Toronto, Montreal, Ottawa, and Winnipeg) showed a similar albeit opposite average change in demand scores -12.4%. This disparity amongst markets resulted in little monthly-over-month movement in average demand scores down only -1.3%.

The varying experiences of the markets within our primary market rankings suggest that there are no overarching themes for this month and that while some markets experienced maintained growth leading into the warmer months, an equal number saw declines in equal proportions.

Average rents continue to trend upwards at a gradual pace, and with the exception of Winnipeg and Edmonton which showed negative monthly growth the remaining markets show an average monthly change of +1.4%. This suggests that even when overall demand slows the general lack of available supply will continue to prompt rent growth.

Primary Market Drill Down (Y/Y): April 2023 vs. April 2022

Notable Changes in Primary Market Demand Over The Past Year

*Year-over-year demand scores are down -15.1%, prospects are down -12.2%, and properties down -20.9%

For the third month in a row, we see a year-over-year decline in renter counts, becoming gradually more exaggerated with each passing month this decline will only continue to worsen. By April 2022 we had long since passed the peak of renter demand for primary markets, each subsequent month will show a trend of gradual declines in renter counts as more and more people successfully completed their rental search. With record low vacancy rates in primary markets, many people who were looking for apartments had already found one now leaving a smaller population of prospective renters.

Unfortunately with a return to tighter market conditions, annual comparisons are becoming less valuable as communities return to an almost frozen state with limited availability and a maintained albeit growing demand for rental apartments.

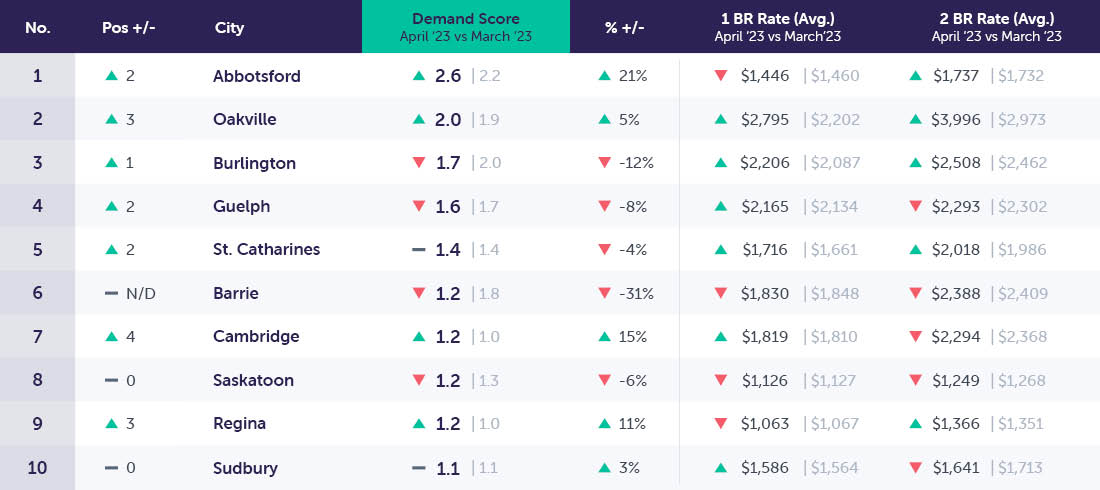

Secondary Markets (Populations ~600-235K)

Secondary Markets Drill Down (M/M): April 2023 vs. March 2023

Notable Changes in Secondary Market Demand Over The Past Month

*Secondary markets demand scores are down -4.7% month-over-month, unique prospects are down -7.4%, and property counts are down -2.8%.

Secondary markets experienced the highest overall decline in demand rates in April with prospect counts declining at a rate 2.6x greater than available properties. These communities are not all in decline however with Etobicoke and Brampton both showing a monthly growth of +16%; while the remaining markets showed varying levels of decline ranging from -1% for Surrey, and -36% in Halifax which showed the single largest monthly decline in rental demand across Canada.

Rent growth was also more muted for secondary markets with a change of +0.33% month-over-month; substantially lower than that of primary markets and that of the broader country.

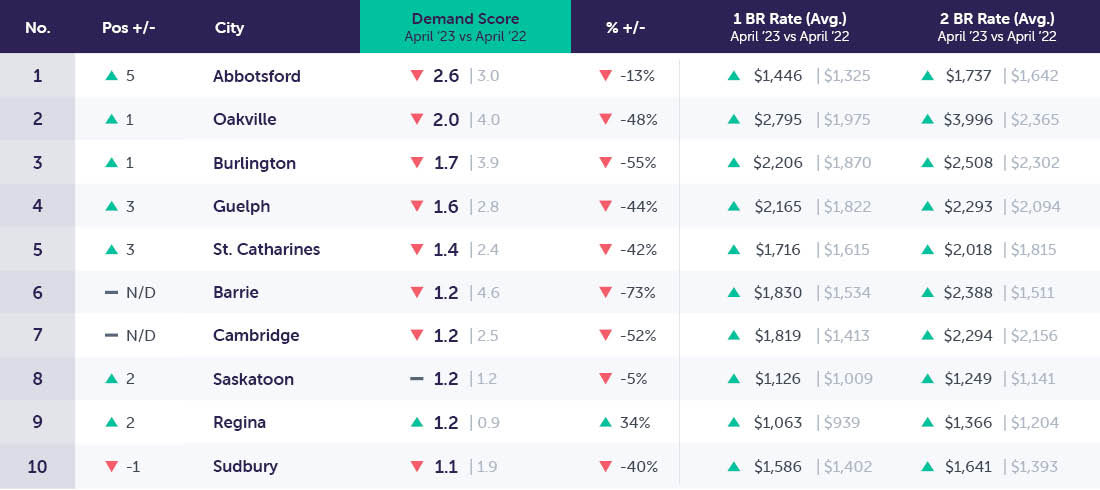

Secondary Market Drill Down (Y/Y): April 2023 vs. April 2022

Notable Changes in Secondary Market Demand Over the Past Year

*Overall, year-over-year demand scores are down -45% year-over-year, with prospects down by -32.3%, and properties down by -5.9%.

As with all annual comparisons, they are disconnected from the reality of current market conditions and do not provide a sufficient explanation for the ongoing trends within secondary markets. These communities are in the process of stabilizing demand patterns after the covid-induced demand in rental demand. Now that many of those who were in the market for rental accommodations throughout 2022 have found a new home these markets are now dealing with record-low vacancies. Although overall market conditions are poorer as compared to April 2022, average prospects per property are down over -28%. The lack of available properties means that competition remains strong for those high-quality properties found on the market.

Although a considerable number of renters have left secondary markets, they remain a serious contender for many renter households looking for access to major markets, while also reducing their cost of living.

Tertiary Markets (Populations ~235-100K)

Tertiary Markets Drill Down (M/M): April 2023 vs. March 2023

Notable Changes in Tertiary Market Demand Over The Past Month

*Demand scores in tertiary markets decreased by -0.1% month-over-month, unique prospects decreased by -2.9%, and available properties decreased by -2.8%.

Tertiary markets experienced the most minimal decline in overall demand scores as renters and available properties declined at a roughly equal pace allowing for overall prospects per property to remain roughly in line with March. March saw an above-average increase in market demand suggesting that these communities may be at the receiving end of an outsized interest amongst new renters entering the market and that these communities may begin to once again lead the pack in regards to monthly gains.

Tertiary markets will continue to attract a dedicated renter population ensuring that properties can attract high-quality renters and fill vacancies.

Tertiary Markets Drill Down (Y/Y): April 2023 vs. April 2022

Notable Changes in Tertiary Demand Over the Past Year

*Overall, year-over-year demand scores are down by -24.7%, unique prospects are down by -8.4%, and available properties are down by -7.0%.

Much of the interest in tertiary markets was gone before March 2022, leading to a year of continued decline in overall demand scores with each subsequent month experiencing a more pronounced decline. Since then these markets alongside the larger primary and secondary markets have stabilized and settled at historically low levels of vacancy leading to limited availabilities and higher relative competition amongst renters.

We will have to continue tracking these communities as they are the closest to potentially experiencing a pinch with properties growing faster than the broader country which creates a more favorable environment for renters.

Conclusion

The rental market experienced a brief slowdown in April, with a dip in overall demand in the first half before showing signs of recovery leading into May. The longstanding trend of tightening market conditions was reversed this month with competition amongst renters actually declining for the first time in recent history. However even with lessened competition those renters still searching for new homes are actually ramping up their activity and submitting more inquiries than before.

This decline is not being felt equally throughout the country, our top 10 markets continue to show strong maintaining power with many showing strong growth even relative to March’s boom in renter demand. This uneven growth requires property owners and managers to ensure they are well positioned with each digital ad campaign is specifically tailored to the market in question in order to maximize reach and strong lead volumes.

As more people continue to head back to work in offices we expect to see the trend of renters being attracted to secondary markets which offer many of the benefits of proximate employment, strong accessibility, and a lower cost of living. Another important point for many renters is walkability with many not willing to compromise on outdoor space post pandemic with many of the communities showing the strongest continued growth being those with ample outdoor space and accessible walking paths.

It is crucial for property managers to stay informed and adapt to changes in the rental market. By staying on top of market-specific trends and implementing effective digital marketing strategies, they can continue to succeed and thrive in the industry. With that said, we encourage all property managers to take action and ensure they are well-prepared for the coming months to maintain a strong position in the market.

To maximize incoming leads and fill available vacancies, consider booking a strategy call with Rentsync to ensure your leasing and marketing initiatives are positioned correctly.

![]()

Methodology

To present this data, Rentsync has determined three key calculations for each area of the report, they are as follows:

Demand Score: Our demand score is rated out of 10 (with 10 being the highest score a city can receive), and is calculated based on unique leads per property, per city, and compared against benchmark data.

For Example Surrey, BC received a demand score of 6.0 this month, versus 6.1 last month. Meaning Surrey experienced a

0.1 point decrease in its demand score.

Demand Percentage (% +/-): This is determined according to the year-over-year (YOY) or month-over-month (MOM) increase or decrease in unique leads per property.

For Example The month-over-month demand scores in Surrey, BC went down -1% in April 2023 versus March 2023, while maintaining the same position within our rankings as the highest-achieving market in April. The year-over-year demand score in Surrey decreased by 2.6 points representing a -30% decrease from April 2022.

Position: The position is determined by unique leads per property, with cities that have at least *20 properties or more. The position will vary depending on demand.

For Example This month, Surrey, BC achieved the top spot on our Top 40 Canadian Cities in Demand rankings, representing a 1 position increase in our rankings from last year.

*This report provides month-over-month rental listing data for April 2023 versus March 2023, as well as a year-over-year comparison from April 2023 versus April 2022. It also outlines the month-over-month and year-over-year trends in primary, secondary, and tertiary markets.