Marketing Managers

Executive Summary

In this comprehensive national rental demand report, we outline significant changes in unique leads per property across Canada. The data presented here is the largest data-backed analysis of rental market demand in Canada using aggregate ILS data (over 20 rental listing sites).

The data included in the Rentsync National Rental Demand Report can be used to compare and contrast demand and lead volume for the properties you manage within a given city and will allow you to make more sound decisions on marketing and advertising.

As you observe demand and unique lead volume percentage, it's possible to measure this against your own metrics, and see whether you are in line with current industry trends, and if not, how to pivot your strategies as a result.

Methodology

In order to present this data, Rentsync has determined three key calculations for each area of the report, they are as follows:

Demand Score: Our demand score is rated out of 10 (with 10 being the highest score a city can receive), and is calculated based on unique leads per property, per city, and compared against benchmark data.

For example: Surrey, BC received a demand score of 10.0 this month, versus 8.0 last month. Therefore, Surrey experienced an increase in its demand score by 2.0 this month.

Demand Percentage (% +/-): This is determined according to the year-over-year (YOY) or month-over-month (MOM) increase or decrease in unique leads per property.

For example: The month-over-month unique leads per property in Surrey, ON went up 25% in January 2022 versus December 2021. In January 2022, the year-over-year unique leads per property in Surrey, ON went up 71% from January 2021.

Position: The position is determined by unique leads per property, with cities that have at least *20 properties or more. The position will vary depending on demand.

For example: This month, Surrey, BC remained in the same position on the Top 40 Canadian Cities in Demand. Year-over-year Surrey, BC is up 1 spot since last year.

*The following report provides month-over-month ILS data for December 2021 versus November 2021, as well as a year-over-year comparison from December 2021 versus December 2020. It also outlines the month-over-month and year-over-year trends in primary, secondary, and tertiary markets.

Key Takeaways:

Month-over-month (M/M): Overall, unique leads per property from December 2021 to January 2022 increased by +21.2%, which represents an unseasonable shift in the first month of the year with growing demand. Supply also increased by 4.75%, resulting in leads per property becoming more substantially more concentrated month over month. The month-over-month market snapshots are as follows.

Month-Over-Month (M/M)

-

Primary: Unique leads per property are up +33.3%

-

Secondary: Unique leads per property are up +8.4%

-

Tertiary: Unique leads per property are up +2.6%

*During this period these markets continue to experience a substantial decrease in available product, while actual demand or inquiries experienced an increase. The unseasonable increase in renter traffic has resulted in unique leads per property values increasing across a majority of individual markets.

Year-over-year (Y/Y): Overall, in Canada, unique leads per property for multifamily residential housing was up +75.65% in January 2022 versus January 2021. This is the result of both a substantial increase in the number of renter inquiry submissions, along with a 36.9% decrease in available supply across all markets as units are absorbed and markets experience a renormalization of their covid induced vacancies. Overall, the year-over-year (January '22 vs January '21) market snapshots are as follows:

Year-Over-Year (Y/Y)

-

Primary: Unique leads per property are up +92.9%

-

Secondary: Unique leads per property are up +99.9%

-

Tertiary: Unique leads per property are up +26.5%

*The year over year analysis indicates that rental demand has maintained an upward trajectory as markets continue to return to pre covid fundamentals and many households are increasingly willing to make housing decisions.

Top 40 Canadian Cities in Demand

*Demand is determined by calculating unique lead volume per property by market. Due to a decrease in available properties in the rental housing market, this report will only highlight the top 40 cities in Canada based on our threshold that requires at least 20 properties to be included in our data sample.

*Please note we have made improvements to our report to better serve readers looking for more in-depth rental market insights.

Notable Changes in Demand Over the Past Month

Overall, Canadian cities experienced an increase in unique leads per property month-over-month (January 2022 vs December 2021). This is likely due to rental supply shrinking by % in comparison to demand, which saw a 21.2% increase in unique leads overall for the month.

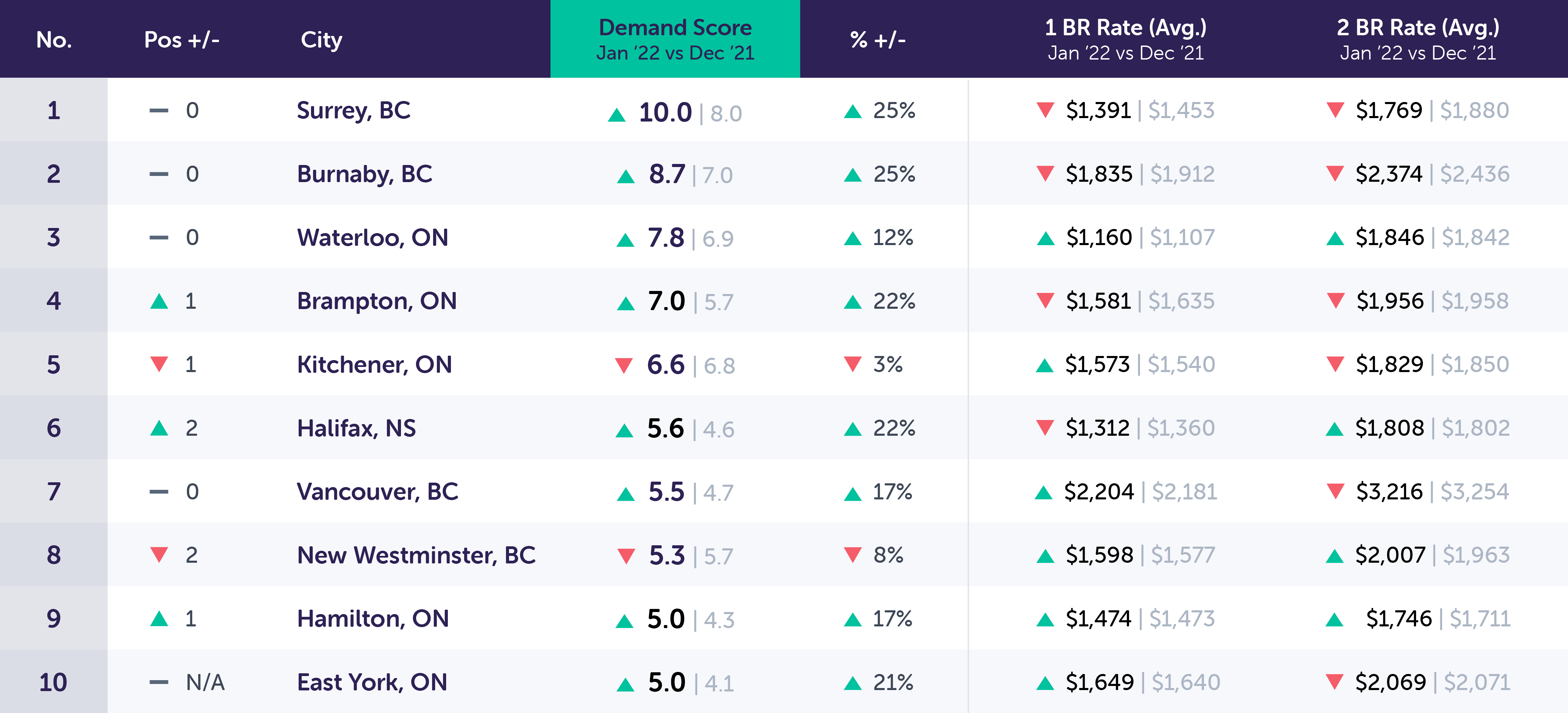

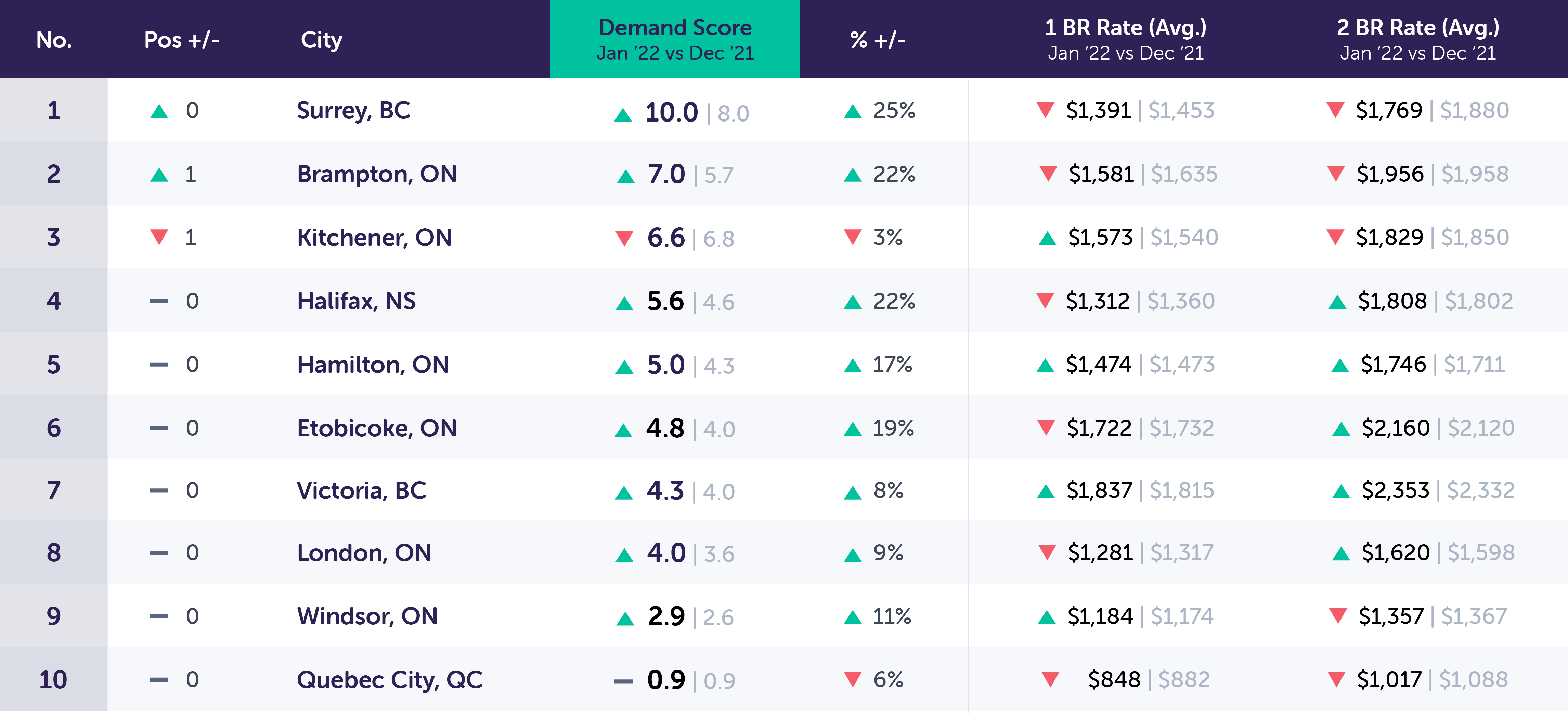

Top 10 Canadian Cities in Demand Drill Down (M/M): January 2022 vs. December 2021

Key Trends for Top 10 Canadian Cities in Demand (M/M)

*Demand scores have maintained relatively consistent month over month, with many continuing to see upward growth, this is a result of supply shrinking from continued leasing, while actual renter inquiries continue to grow. Although typically a shrinkage of lead volume is expected in January, the continued return of many renters to the housing market has continued the trend of inquiry growth which is likely to be maintained as markets recover.

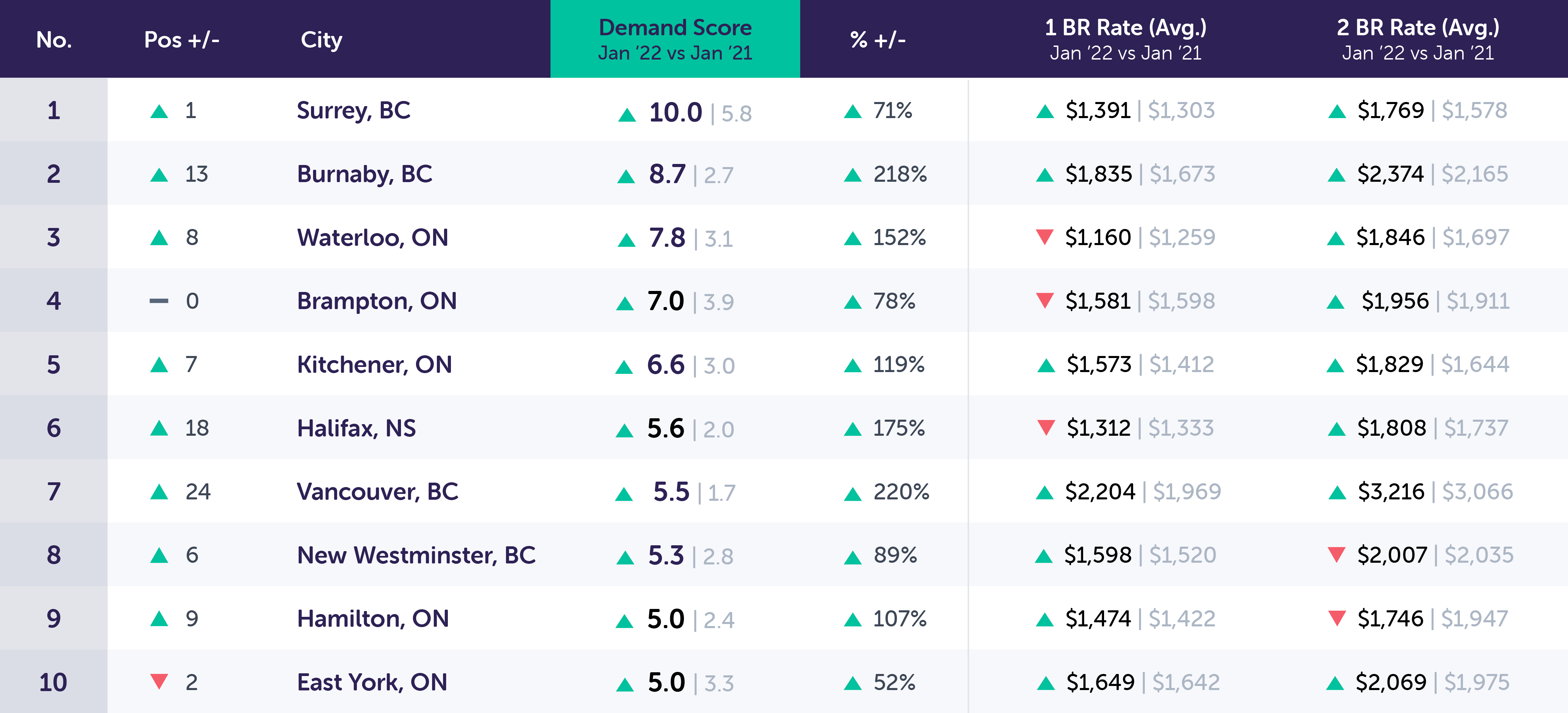

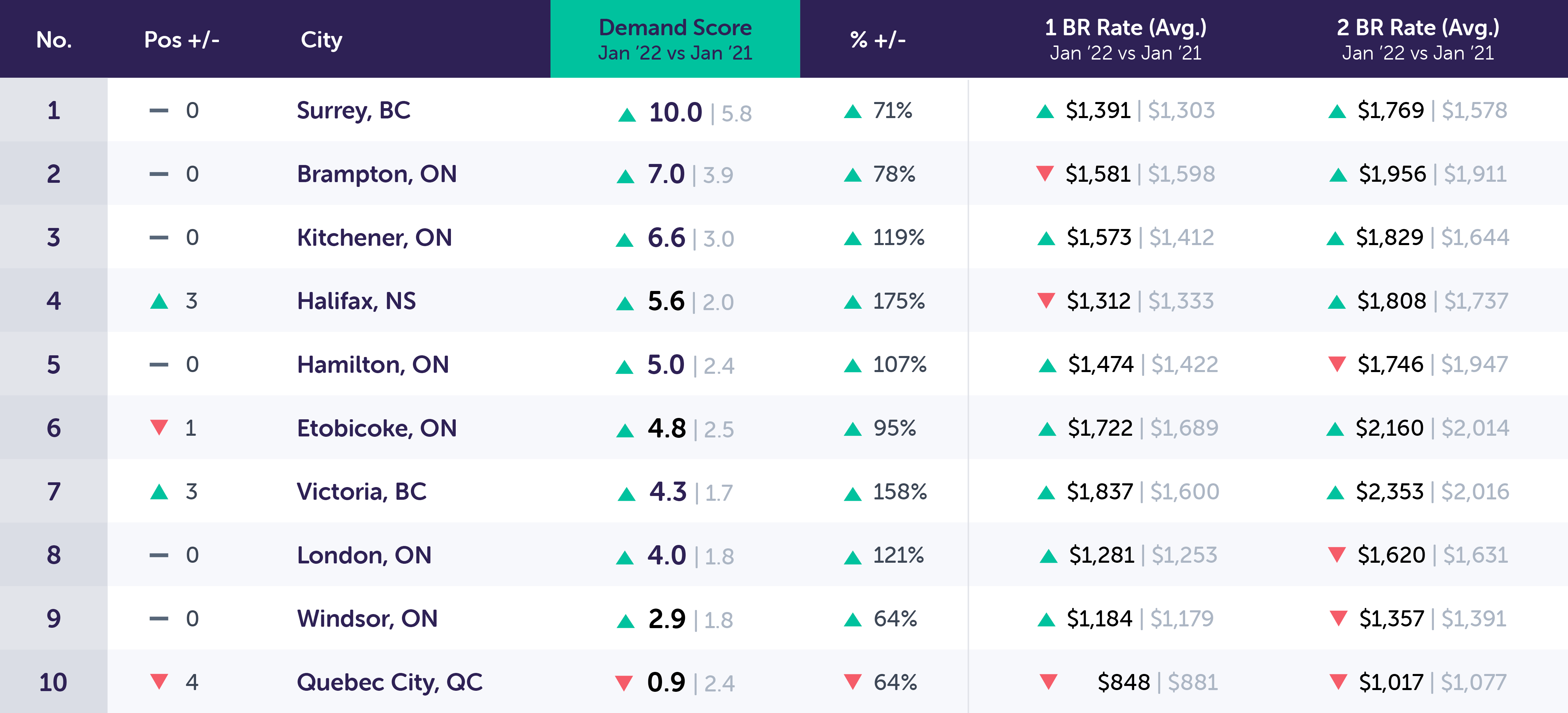

Top 10 Canadian Cities Drill Down (Y/Y): January 2022 vs. January 2021

Key Trends for the Top 10 Canadian Cities in Demand (Y/Y)

*Again we see the continued long term normalization of renter traffic and apartment inquiries. The biggest gainers throughout this period remain secondary markets with significant long term and continued growth in renter traffic, however there are primary markets which are undergoing a similar resurgence, specifically Vancouver which has experienced the highest relative increase year-over-year in renter traffic of 220%. This resurgence in Vancouver is also highlighted by the highest relative growth in achievable rental rates as properties are increasingly less reliant on price competitiveness in order to attract renters.

January has seen the continuation of the trends experienced in Q4 of 2021 namely being the continued tightening of available supply, and growing resurgence of markets other than smaller tertiary communities. With a majority of the units left vacant throughout covid having been reabsorbed by residents returning to the rental market we see a tightening of market conditions which has resulted in strong rent growth. Many markets especially major regional economic hubs such as Toronto, Hamilton, Kitchener, and Vancouver have regained a majority of the rent loss experienced throughout 2020 and 2021 which suggests that they are likely to return to pre-covid rental rates in the foreseeable future.

The trend of many moving away from primary markets has lessened to an extent with smaller tertiary markets representing the largest overall share of inquiry loss as households return to primary and secondary markets for their improved amenitization and quality of life. This does not however negate the value posed by tertiary markets as they remain strong attractors for young families and will continue to be in high demand as many continue to be priced out of major housing markets through increased rental rates and real estate prices.

An Analysis of Key Canadian Markets

In order to better segment our data and analyze what is happening within specific markets across Canada, we have broken down our data into 3 key market segments:

-

Primary (Populations Over 600K)

-

Secondary (Populations Between 600-235K)

-

Tertiary (Populations Between 235-100K)

Here we will gain a deeper perspective on demand across larger populations and any movement due to the impact of COVID-19 on the rental market.

Key Takeaways:

Both the supply of available units, and the demand posed by prospective renters has seen a gradual decrease; however, the relationship between the two is disparate with supply decreasing at a higher relative rate. This has enabled the overall leads per property figures to show an overall increase.

Month-Over-Month (M/M)

-

Primary: Unique leads per property are up +33.3%

-

Secondary: Unique leads per property are up +8.4%

-

Tertiary: Unique leads per property are up +2.6%

Year-Over-Year (Y/Y)

-

Primary: Unique leads per property are up +92.9%

-

Secondary: Unique leads per property are up +99.9%

-

Tertiary: Unique leads per property are up +26.5%

Primary Markets (Populations >600K)

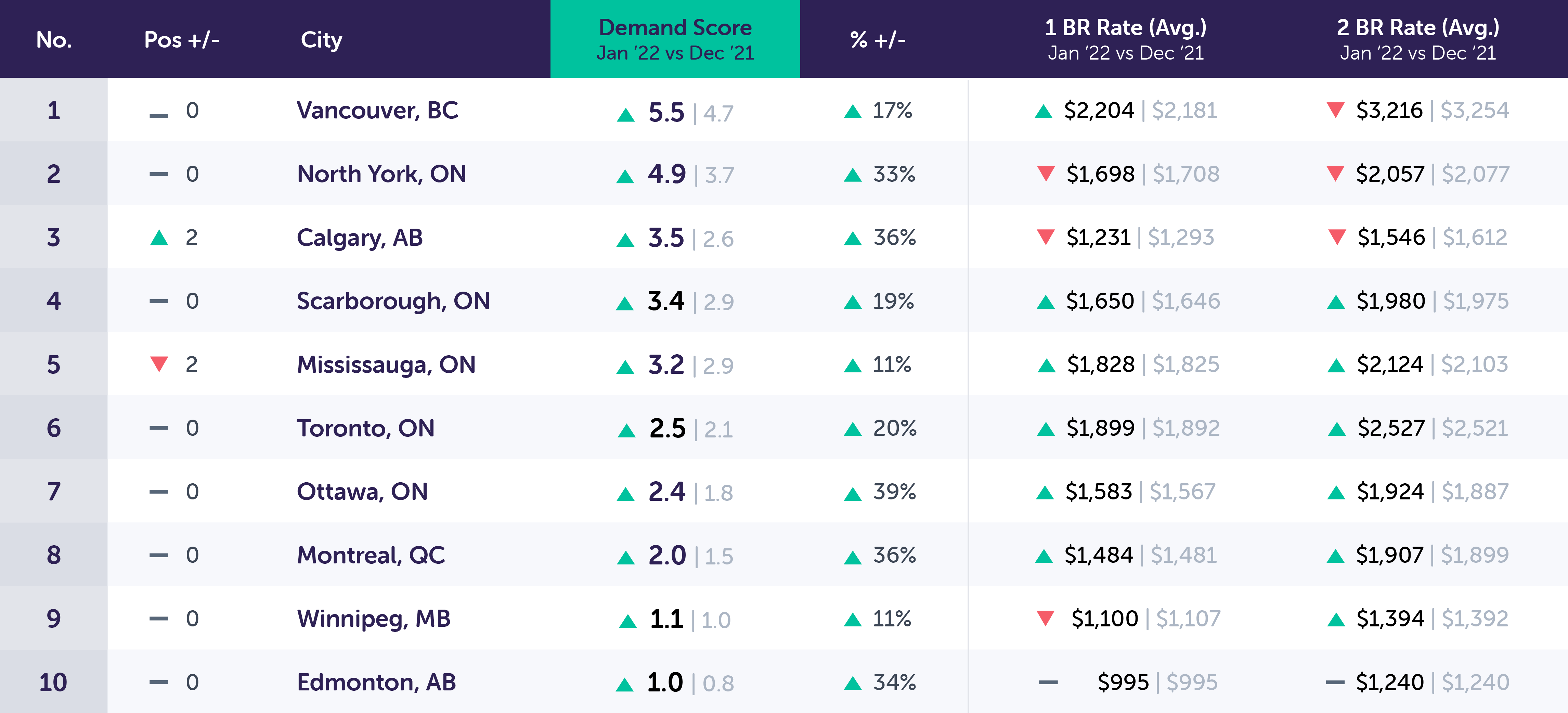

Primary Market Drill Down (M/M): January 2022 vs. December 2021

Notable Changes in Primary Markets Over the Past Month

*Unique leads per property in primary markets saw a substantial increase this month. Overall unique leads per property increased by +33.3% in primary markets this month.

Market fundamentals continue to return to their pre-covid states. Unlike in the previous month both inquiry volume, and unit availability increased substantially for primary markets which has resulted in demand score growth across the board. These markets are the biggest gainers as covid restrictions are further loosened in advance of total removal and residents return in search of more convenient urban living. The slowly shrinking availability and continued growth in inquiry volumes suggests that these markets are accelerating towards full stabilization from covid induced instability.

(See the year-over-year analysis below, for more perspective on demand in primary markets.)

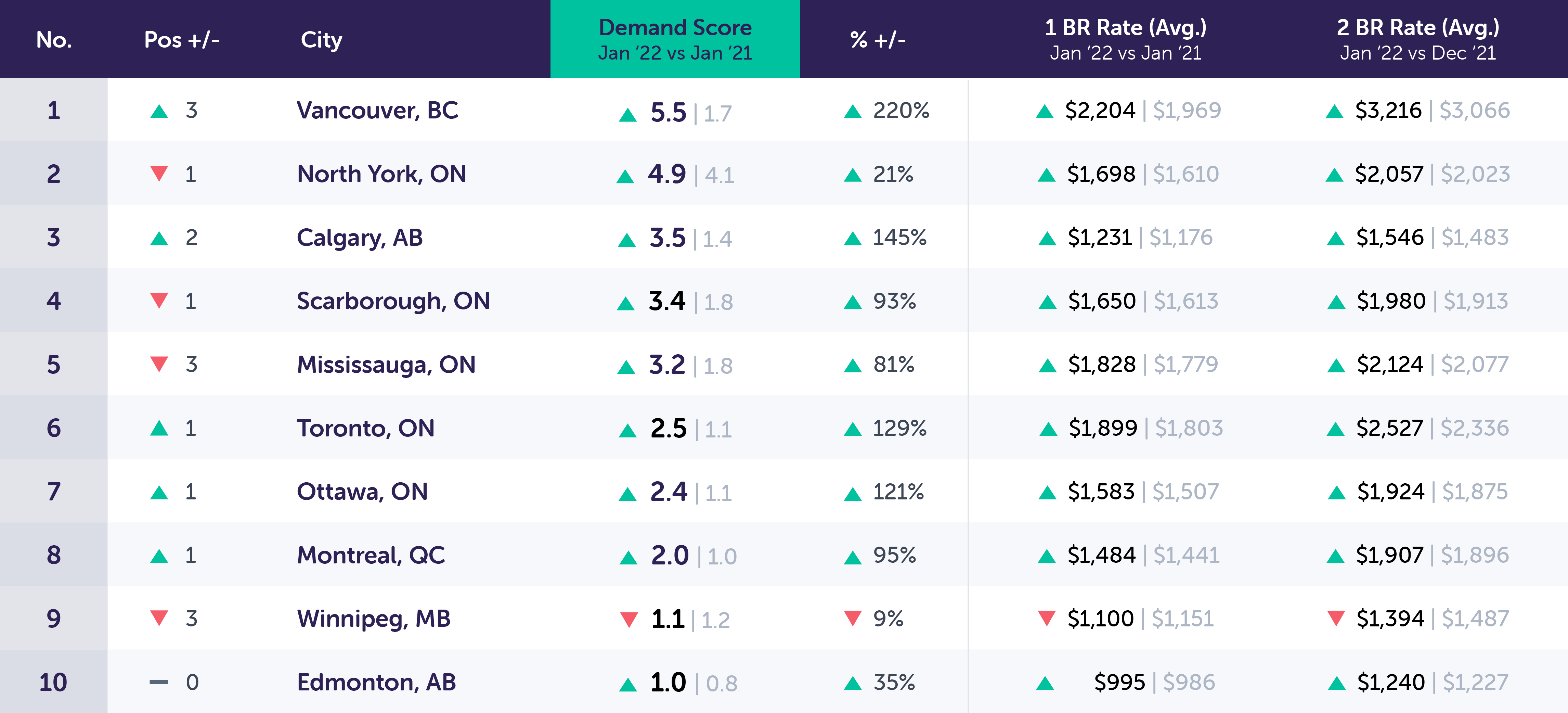

Canadian Cities – Primary Market Drill Down (Y/Y): January 2022 vs. January 2021

Notable Changes in Primary Market Demand Over the Past Year

*Overall, year-over-year primary market unique leads per property continues to rebound versus the same time last year and have increased +92.9%. The omicron wave had little effect on renters' willingness to continue their search for new housing as the overall trend shows a substantial return to key markets by renters. Although restrictions were present in some communities, the inquiry volume showed limited stagnation with substantial growth year-over-year.

Alongside the growing demand for apartments, we also experience growth in rental rates which suggest that not only has demand rebounded, but that market conditions are gradually returning to those experienced prior to covid and that incentives are likely to gradually disappear as competition for renters declines. This has allowed for the continued growth and acceleration of rental rates within metropolitan areas after over a year of stagnation. This is however not a perfect picture as markets such as Winnipeg which was particularly hard hit continue to experience the effects of the slowdown in renter demand and will likely require an extended rebounding period as both inquiry volume and rental rates continue to contract.

Secondary Markets (Populations ~600-235K)

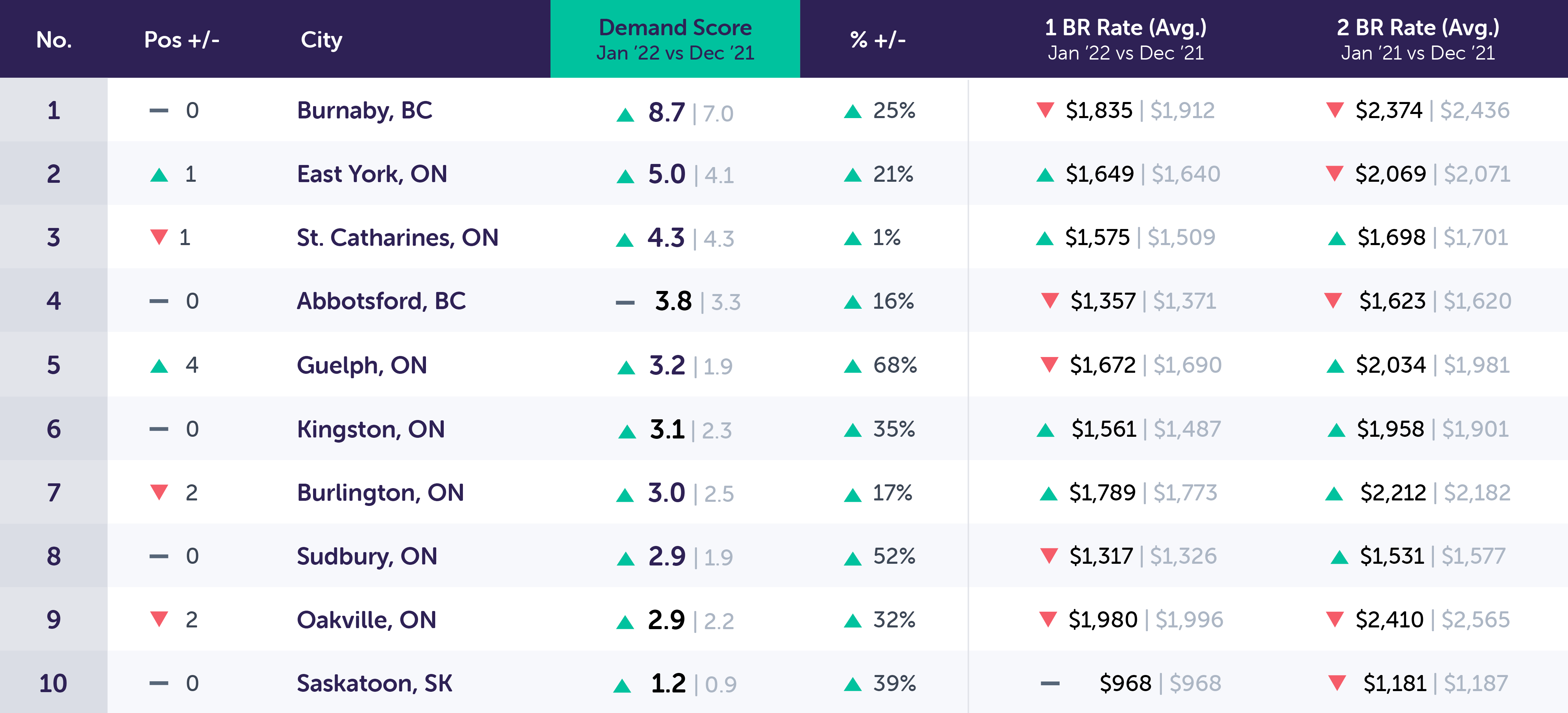

Secondary Markets Drill Down (M/M): January 2022 vs. December 2021

Notable Changes in Secondary Market Demand Over the Past Month

*Secondary markets saw an increase of +8.4% unique leads per property this month. These markets saw the least amount of movement in January with an overall increase of approximately 20% inquiries, and 5% greater availability month over month.

Although demand remains strong within these markets, many are not immune to over pricing as some markets experience price corrections with an average price fluctuation of -1.4% month-over-month. Although rents remain up year-over-year this price fluctuation may suggest that the push for smaller outlying communities is beginning to falter and that more competitive pricing may be in part due to a stabilization of overall demand trends.

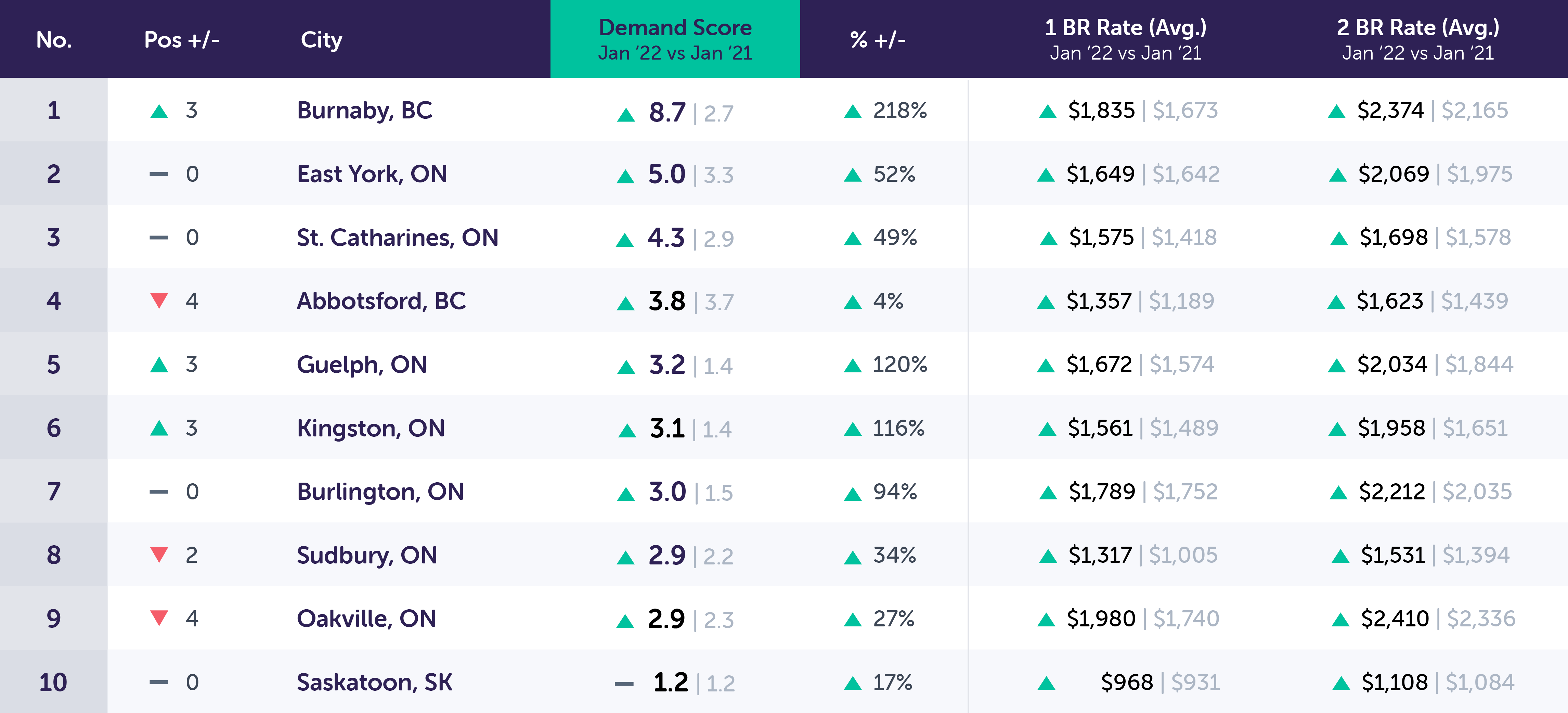

Secondary Market Drill Down (Y/Y): January 2022 vs. January 2021

Notable Changes in Secondary Market Demand Over the Past Year

*Overall, unique leads per property are up +99.9% in secondary markets this year versus this time last year. The significant year-over-year increase suggests that secondary markets are the biggest largest earners over the previous 12 months with substantial growth in unique leads per property. Although demand has slowed more recently, this significant growth is likely to bring long term benefit to these communities through the influx of new households competing for the limited existing rental stock.

The markets which have experienced the greatest overall levels of growth are primarily those who are not reliant on a geographically proximate major market for employment and instead contain their own business districts with sufficient employment opportunities. This has resulted in markets like Halifax, Hamilton, Kitchener, London, and Victoria to not only experience substantial growth in the overall demand for rental, but have also benefited from on-going rent growth. This may be an interesting trend to continue watching into the future as it suggests that these markets are likely to continue to benefit from this growth.

Tertiary Markets (Populations ~235-100K)

Tertiary Markets Drill Down (M/M): January 2022 vs. December 2021

Notable Changes in Tertiary Market Demand Over the Past Month

*Unique leads per property increased by +2.6% this month versus last month in tertiary markets.

Tertiary markets were the least immune to the January slowdown with a limited growth to unique leads per property. However this was not due to a shortage in unique inquiries and instead linked to the greater relative supply of available units. In addition many markets experienced a contraction in achievable rents which suggests that regardless of seasonality they are experiencing a stabilization in market conditions and a return to pre-covid conditions. These communities will continue to diverge moving forward and are likely to display disparate levels of growth and associated market conditions well into the future based on broader macroeconomic conditions.

(See the year-over-year analysis below, for more perspective on the rise in demand in tertiary markets.)

Tertiary Markets Drill Down (Y/Y): January 2022 vs. January 2021

Notable Changes in Tertiary Demand Over the Past Year

*Overall, unique leads per property are up in tertiary markets +26.5% this year versus the same time last year. Year-over-year tertiary markets continue to show strong signs of growth and migration due to more affordable housing and remote work.

Although tertiary communities experienced gains throughout the pandemic in regards to increasing rental demand, some of this growth has receded indicating some of the appeal which had attracted many households has dissipated and many are now looking to return to larger markets. This trend is most evident in rural communities as opposed to those which are within commuting distance of a major market or offer proximate employment opportunities. Regardless, the overall trend of households' willingness to move into smaller communities persists to a smaller extent and is likely to continue as a staple within the Canadian rental industry moving forward.

Conclusion

The data shown in this report suggests that this month that Canadian rental markets have remained consistent from December to January, with close to no seasonal decline in unique prospects per property, and strong upward growth in total inquiries. The increase in unique leads per property is unseasonal for the month of January, as we typically see a major reduction of demand throughout the holiday season and the first few months of the year, but it can be concluded the willingness of a substantial number of Canadians to reopen and re enter society has lead to an overarching trend of increasing demand for apartments.

that as restrictions remained loose in December, and supply remained scarce, this caused a relative increase in unique prospects per property for those available on the market.

Vacancy rates in urban areas such as Toronto have dropped from 6.4% in Q1 of 2021 to 3% in Q3; and with less supply available, continued upward growth in total unique leads,lead volume is becoming much more concentrated.

These factors suggest that with an unseasonably high traffic of rental inquiries we are likely to see a year of renewed market fundamentals, a return to major markets, and ongoing growth in rental rates. The resurgence of major markets will be compounded by the already speculative nature of real estate in these communities to create significant demand across all property classes and the overall demand for purpose-built rental is likely to continue to grow.

We will continue to monitor, and provide an in-depth data analysis, month-over-month, and year-over-year to provide you with the most accurate insights that can help to support your ongoing marketing and advertising strategies, especially as we navigate through these unprecedented times.